I started to write a post about dealing with goodwill calculations in getting to an invested capital number for ROIC and I then realized that to do that well, I need to go back and provide context for intangible assets in general, from economic and accounting standpoints. My hope is that the next few posts will be kind of a top-level resource on intangible assets to set the stage for future posts about specific companies and how to think about their intangible assets when trying to get a handle on their capital productivity.

The broadest definition of an intangible asset is something that lacks physical presence but that provides economic value. That can be almost anything, from a great company name or URL to a customer list, an employee manual, or even the knowledge of customers that exists only in an employee’s mind. It’s a wide spectrum of possibilities, but let’s start with the part of the spectrum that is most concrete – that’s what I refer to as Intellectual Property According To the Lawyers.

Intellectual Property According To The Lawyers

4 Categories:

- Patents – The U.S. Patent and Trademark Office grants property rights to original inventions, copyrights, and trade secrets. Hire a patent lawyer, apply for, and receive a patent so that your competitors can’t knock off the product you invented.

- Trademarks – Protect logos and symbols used by a company via the U.S. Patent and Trademark Office.

- Copyrights – Protect the original creator of some kind of work product that does have physical presence (i.e. it’s not just an idea), like a song or a literary work. Registration with U.S. Patent and Trademark Office is not required but is advised so that the creator timestamps the date of creation for use in any litigation that may ensue.

- Trade Secrets – Business ownership of a formula, pattern, compilation, program, device, method, technique, or process that provides a competitive edge. As a member of the World Trade Organization, the U.S. government has a responsibility to protect trade secrets. The passage of the Defend Trade Secrets Act of 2016 (DTSA) also increased trade secret protection. Under the DTSA, an individual or organization may be found liable in a civil case for the misappropriation of trade secrets.

If one were to rank the quality of intangible assets with respect to creating competitive advantage and sustained economic profits and intrinsic value for a business, these would be at the top of the list. Any valuable intangible asset that is explicitly protected by the law is the kind you want.

Non-Lawyer Defined Intangible Assets

Then there is the other stuff. Here are some examples, but this list is by no means exhaustive:

- Customer lists

- Process & Employee Knowledge, Employee Talent (kinds of Human Capital)

- Culture

- Brands (a brand can be protected by a Trademark but is often far more valuable, so brand value is often an intangible asset that exceeds how the trademark may be valued)

- Software and other tech assets that are not computer hardware

- Critical supplier and customer relationships

- Training processes/manuals

- Capitalized R&D (accounting discussed later)

- Mineral rights

- Supply contracts, purchase agreements

- Franchise agreement rights

- Government or other key contracts

- Reputation

Here is how Baruch Lev at NYU Stern categorizes all types of intangible assets in his presentation The Wonderful World of Intangibles (2015).

The Major Categories of Intangibles

| Discovery/Learning: | Patents on new products and services, communities of practice, adaptive capacity |

| Customers: | Brands, trademarks, on-line distribution channels, marketing alliances |

| Human Resources: | Unique work and compensation practices, employee training, incentives/compensation arrangements |

| Organizational Structure: | Business structures and processes, incentive systems, information and control systems. |

And here is how Michael Mauboussin cuts it up in One Job (2020). As the footnote shows, he got it from Capitalism without Capital: The Rise of the Intangible Economy:

We can see that regardless of how one categorizes them, these kinds of assets make intuitive sense to track and get to know. They are critical for making products and providing services, and ultimately driving profits. In fact, it’s hard to imagine any kind of reasonably successful business not possessing and using these assets. It’s a great idea to try to be cognizant of these buckets as a kind of checklist when looking at a business and thinking: “This appears to have high returns, but what is driving it exactly, and how sustainable is that and how much re-investment does it require?”

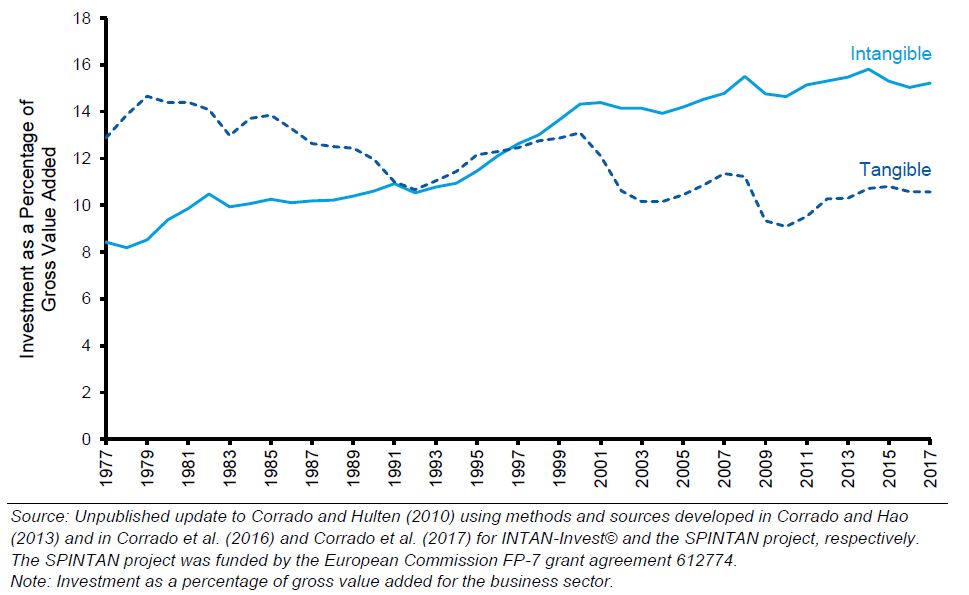

Growing Prevalence & Importance Of Intangibles

In recent years, companies are investing far more in intangible assets than tangible ones, which is consistent with how large a role technology has come to play in all of our lives. Some numbers on this, again from One Job:

Intangible assets also have unique characteristics over tangibles for a business, including that they are more scalable, leverage network effects better, and are more reliant on human capital. This is discussed in detail in Capitalism without Capital and it’s a popular topic for finance and accounting academics lately. It’s also an important consideration for anyone interested in valuation or digitization trends in business. This will be the subject of a future post but in the meantime here are more resources for the growth of intangible asset investment by companies:

The Wonderful World of Intangibles, Baruch Lev 2015

Valuing Intangibles, Aswath Damodaran 2009

Intangibles and Earnings, Michael Mauboussin 2022

The Impact of Intangibles on Base Rates, Michael Mauboussin, 2021

Intangibles, Investment, & Efficiency, Nicolas Crouzet 2018

In the next post on accounting for intangibles, we’ll get into accounting and some of the arbitrary measurements of intangible assets under GAAP and IFRS. An accounting-defined intangible asset can be vastly different from how we think about an intangible asset in economic terms, if the asset is even recognized by accounting at all. This arbitrariness must be understood to get useful reads on ROIC, since ROIC really does rely heavily on accounting.

Leave a Reply