What is a good rate of return? Well, the way Greenblatt does this is via a system in which stocks are ranked based on their combined score for good business and good price – so basically a good business is a relatively good business compared to other publicly traded stocks. In some years, this could mean 25% is “good,” and in others, it could mean 7% is “good,” it all falls out of the rankings. But the way most investment professionals think about the rate is far more casual – they look at the ROIC in terms of opportunity cost: how good is the number vs. the risk-free rate plus some kind of risk premium for this particular stock or just simply, does it get them excited, because economic profits are very exciting? Of course, public companies live by the same risk-free rate and an equity risk premium which is just a type of risk premium, so this is all interrelated, and I will get much more into the details here in a later post. Incidentally, Aswath Damodaran, whose work I will reference often on the blog, has a great website with lots of data, and it includes implied equity risk premium calculations going back to 1960. It is located here. He pegs the implied equity risk premium at 4.9% as of January 1, 2022. If the 10-year Treasury is 1.8% that gets you to an opportunity cost of about 5.7%.

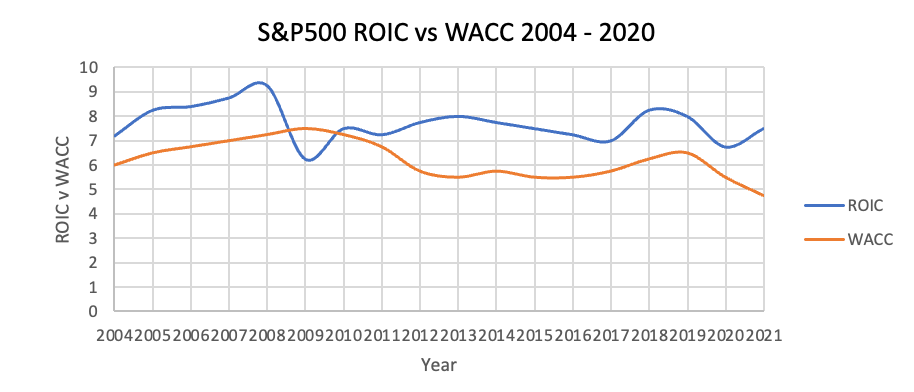

Below is a simple time series of the ROIC of the S&P 500 vs. its cost of capital from 2004 through 2020:

Source: Bloomberg

You can see the WACC (weighted average cost of capital) of the S&P 500 is in the same range as the rough math done above for opportunity cost. The S&P 500 also has an ROIC in the high single digits (depending on which ROIC formula is used, whether or not non-profitable companies are excluded, how the weighting is being done, which sectors may/may not be included…) so suffice it to say that an ROIC for a stock probably starts to become the kind of thing you would be interested in and highlight in a pitch at double that level, or say 15%+. If you need a number, there you go. Of course, 10% could be great too, depending on valuation, reinvestment rate, and your sense of the overall risk of the cash flows related to the business you are looking at – all topics for another day.

These numbers have been remarkably consistent (since 2004, at least), and there is a much broader conversation around their relationship to the risk-free rate and the Equity Risk Premium that becomes more important if one expands the time series by a few more decades to see what happens when these numbers vary a lot from what they were in 2004-2021 (i.e., the world before Greenspan and very low rates).

But, this provides a good, back-of-the-envelope starting point benchmark for the “what’s a good number” question. Also, remember that it’s not just the magnitude of the ROIC or economic profit level, but also its sustainability (AKA fade rate) that drives intrinsic value for a business. Having a good handle on both of these is critical, and not easy, as doing that involves a fair amount of predicting the future. But that’s what you get paid the big money for. I plan to devote several blog entries to the sustainability issue, because it may be the single most important aspect of ROIC analysis as it related to valuation and stock picking.

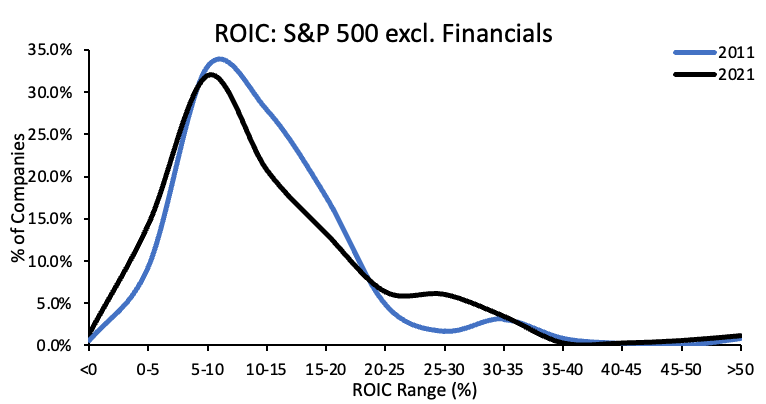

How common is it to find companies that put up significantly higher ROICs, at least for a given year? Below is a chart that shows the distribution for the S&P 500 in 2011 and 2021.

Source: Portfolio123.

Note there is no market cap weighting here, it’s just the number of companies. The distribution in these two years was very similar, despite the fact that they were a decade apart – and that was a decade of a lot of digital disruption. The number of companies with solid but not super-high ROICs seems to have gone down from 2011 to 2021, while the number in the 20-35% range went up. It would be great to see the data on which and how many companies kept the same or improved ROIC during this time period, or if the distribution remained about the same but the companies changed significantly. My guess is that most of the same mega-tech companies with high ROICs probably stayed to the right on the X-axis due to some of the big-tech, anti-competitive stuff that has been in the news lately, while the rest changed fairly dramatically. If you have the data or know where to get it, please share!

At any rate, this graph shows the simple fact that companies with ROICs above say 20% for even one year are pretty rare. In the next post we will start getting into exactly how to calculate ROIC.

Leave a Reply